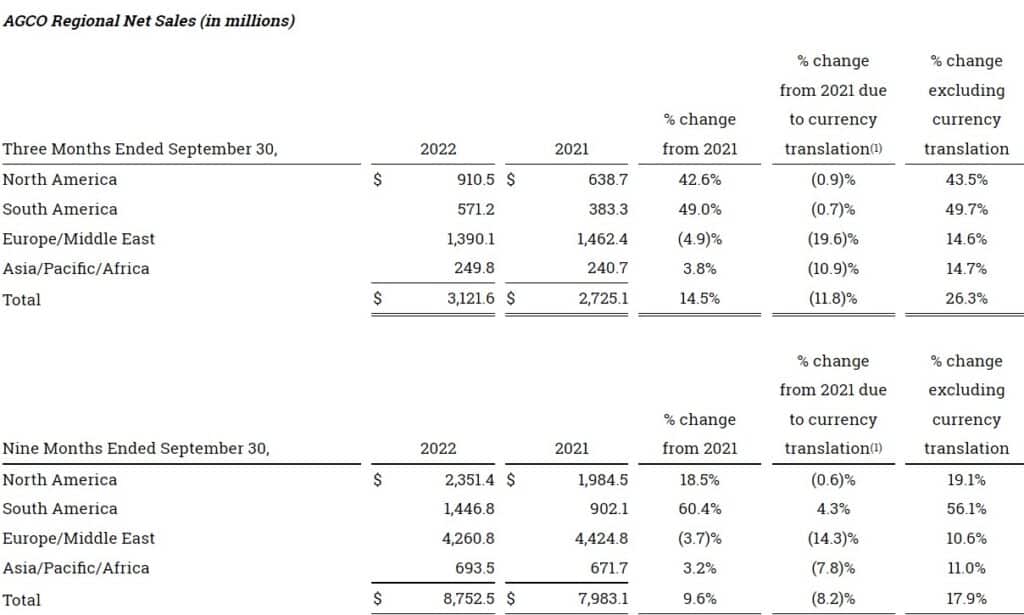

AGCO reported its results for the third quarter ended September 30, 2022. Net sales for the third quarter were approximately $3.1 billion, an increase of approximately 14.5% compared to the third quarter of 2021. Excluding unfavorable foreign currency translation of approximately 11.8%, net sales in the quarter increased approximately 26.3% compared to the third quarter of 2021.

“We delivered record third quarter sales and earnings driven through the consistent execution of our farmer-first strategy, coupled with continued robust market conditions in many of our regions,” stated Eric Hansotia, AGCO’s Chairman, President and Chief Executive Officer. “Our solid operational performance and continued strong pricing overcame ongoing supply chain challenges, inflationary pressures and significant currency headwinds. Healthy farm fundamentals are supporting order boards that now stretch well into 2023 in some regions. The success of our farmer-first strategy, focused on growing our precision ag business, globalizing a full-line of our Fendt branded products and expanding our parts and service business, is generating strong growth in these margin-rich businesses.”

Mr. Hansotia continued, “Global market conditions remain positive as favorable farm economics are allowing farmers to upgrade and replace their aging fleets. At the same time, our smart technology product lines are in strong demand and are helping to drive meaningful productivity improvements for our customers through both retrofitting their current equipment and in our new product offerings. We will continue to accelerate investments in premium technology, smart farming solutions and enhanced digital capabilities to support our farmer-first strategy while helping to sustainably feed the world.”

Net sales for the first nine months of 2022 were approximately $8.8 billion, an increase of approximately 9.6% compared to the same period in 2021. Excluding unfavorable foreign currency translation of approximately 8.2%, net sales for the first nine months of 2022 increased approximately 17.9% compared to the same period in 2021.

“Healthy farm income is projected across most of the major agricultural production regions with elevated crop prices offsetting higher fuel, fertilizer and other input costs,” stated Mr. Hansotia. “Despite ongoing supply chain disruptions, favorable farm economics are expected to generate strong demand across all the major global markets well into 2023.”

Global industry production and retail sales were down modestly in the first nine months of 2022 compared to last year’s elevated levels due primarily to supply chain limitations. Industry retail sales for tractors in North America were down approximately 6% in the first nine months of 2022 compared to last year. The decline was driven by weaker sales in smaller tractors partially offset by improved sales of high horsepower tractors, which increased approximately 8% in the first nine months of 2022 compared to the same period in 2021.

Regional differences

In Western Europe, industry retail tractor sales decreased approximately 10% in the first nine months of 2022 compared to strong levels in the same period of 2021. Farmer sentiment in the region has been negatively impacted by the conflict in Ukraine, looming energy concerns, and higher input cost inflation. Forecasts for healthy farm income in Western Europe are expected to support relatively flat retail demand for equipment in the fourth quarter of 2022.

South American industry retail sales increased during the first nine months of 2022 in both Brazil and Argentina compared to 2021 levels. Healthy farm income, supportive exchange rates and continued expansion in planted acreage are driving increased investments in high tech farm equipment.

“Disruptions in the global supply chain are continuing to limit industry production; however, we continue to expect strong demand in the fourth quarter to support full year 2022 industry retail sales above 2021 levels in South America, relatively flat sales in North America and modestly lower sales in Western Europe,” continued Mr. Hansotia.

North America

Net sales in the North American region grew 19.1% in the first nine months of 2022 compared to the same period of 2021, excluding the negative impact of currency translation. The increase resulted primarily from increased sales of tractors and precision planting equipment along with the effects of pricing to mitigate inflationary cost pressures. Income from operations for the third quarter of 2022 was approximately $76.9 million higher compared to the same period in 2021, which drove an increase in income from operations for the first nine months of 2022 by approximately $3.8 million compared to 2021. Operating income benefited from higher sales and production, but was mostly offset by material and logistics cost inflation, higher production costs and increased operating expenses.

South America

South American net sales increased 56.1% in the first nine months of 2022 compared to the same period of 2021, excluding the impact of favorable currency translation. Sales grew strongly across all markets, driven by robust industry demand and favorable pricing impacts. Income from operations in the first nine months of 2022 increased by approximately $155.4 million compared to the same period in 2021, and operating margins reached approximately 16.5%. The improved South America results reflect the benefit of higher sales and production, pricing in excess of material cost inflation and a favorable sales mix.

Europe/Middle East

Europe/Middle East net sales increased 10.6% in the first nine months of 2022 compared to the same period in 2021, excluding unfavorable currency translation. The improvement was driven by higher sales of tractors and replacement parts along with favorable pricing actions. Strong growth in France, Turkey, Central Europe and Scandinavia accounted for most of the increase. Income from operations decreased approximately $72.5 million in the first nine months of 2022, compared to the same period in 2021. The decline was the result of foreign currency translation, a weaker sales mix and higher production costs.

Asia/Pacific/Africa

Net sales in Asia/Pacific/Africa increased 11.0%, excluding the negative impact of currency translation, in the first nine months of 2022 compared to the same period in 2021. Higher sales in Australia and Africa were partially offset by lower sales in China. Income from operations improved by approximately $21.5 million in the first nine months of 2022 and operating margins expanded by approximately 2.7% compared to the same period in 2021 due to higher sales and a richer sales mix.